Chinese market represents ‘single greatest generational opportunity’ for Pharma

China’s pharmaceutical industry is changing from formerly generics-focused into one that emphasizes innovation, spurred by shifting government policy and an aging population.

In this article, we will take stock of China’s innovation ecosystem, look at the key trends driving the biopharma industry, and assess opportunities for multinationals operating in the world’s second largest pharma market.

Pricing and market access

For innovative therapies in the Chinese market, access and affordability have always represented significant roadblocks. The uptake of innovative drugs tends to be much slower in China than in other markets due to access challenges such as provincial tendering, hospital listing, and patient affordability gaps[i]. However, this landscape is changing and, thanks to a number of government initiatives in recent years, market access and pricing conditions are becoming more favourable for companies attempting to bring innovative drugs to China.

Market access

Initiatives such as the Hainan Boao Lecheng International Medical Tourism Pilot Zone (also known as Hope City) and the Medicine Connect programme have made significant strides to ease market access constraints. Hope City, located in Hainan province, is the first and only international medical pilot zone in China with exclusive preferential policies. In short, this means that patients can be treated with drugs, devices, and innovative therapies that have been approved overseas, but not yet in China[ii]. Sometimes making a debut in Hope City will facilitate later approval by the National Medical Products Administration (NMPA), as was the case for Takeda’s plasma kallikrein inhibitor Takhzyro in 2020[iii].

The Medicine Connect programme is a similar pilot for the Greater Bay area endorsed by the NMPA and seven other regulatory bodies. The programme allows designated mainland hospitals to use drugs and medical devices approved in Hong Kong and Macau without prior NMPA approval[iv]. In April 2021, RhoGAM (anti-D immune globulin) became the first therapy approved for use in the Greater Bay area through the programme[iii], and more than 13 drugs and four medical devices have been approved since[iv].

Pricing

Drug pricing remains a central factor when talking about the shift towards innovation in the Chinese pharma market. In order to access much of the Chinese market, drugs must be included on the National Reimbursement Drugs List (NRDL). Inclusion on this list means that products will be fully or partially reimbursed at the national level and are generally the only products to be prescribed from public hospitals[v]. Previously, generics made up most of this list and domestic manufacturers were favoured over foreign companies. However, the transformation of the NRDL since 2017 has been substantial - after eight years without updates, China agreed that as part of the Healthy China 2030 policy the NRDL would be updated annually. Since then, approximately 300 innovative drugs have been added to the list, which contains more than 1,486 ‘Western’-made medicines and 1,374 Chinese-patented medicines[v]. In 2020, manufacturers were given the option of being able to apply for NRDL inclusion, whereas before they had to wait for selection.

Another initiative that’s had a substantial impact on pricing and access is the Volume-Based Procurement (VBP) program, which launched in 2018. This program aims to establish generic quality consistency evaluation (GQCE), reduce generic drug prices and consolidate the fragmented system for procuring generic drugs. Since then, four successful rounds of the VBP program have streamlined generic drug prices and introduced a quality control system within the Chinese pharma industry[vi].

Both the NRDL and VBP have put pressure on companies’ profit margins, prompting many to shift their focus towards R&D and innovation.

According to Vicky Xia, Head of Beijing BioPlan Associates, pricing represents the greatest challenge for innovators in the biopharma space.

‘Market demand is on the rise due to rising accessibility and there are multiple government programmes trying to control drug prices. And as a result, access to drugs which are considered relatively high-end will increase and the overall market will expand, but profit margins will definitely decrease,’ she tells CPHI.

‘It's a complicated scenario. Not all the moves are good, but there are still opportunities out there.’

David Deere, President of BioVane Inc, agrees that the pricing environment represents challenges for domestic and foreign firms alike, as companies are often forced to choose between slashing their prices or being locked out of major segments of the market.

‘Inclusion on the NRDL mandates, on average a 50% reduction in price. When a drug goes through two rounds on the NRDL, the price is sometimes down over 90% from when it was introduced five or six years earlier, it takes it down fast. And that's an issue that the multinationals are going to have to specifically target in China - can they play with innovative drugs in that dynamic of a market?’ Deere says.

Up until the NRDL was introduced in 2017, multinationals made most of their money selling old, branded drugs at a premium price in China. When volume-based discounts were introduced for generics, branded drugs were pushed out and multinationals were forced to start introducing innovative products.

‘China is by far the singular largest market opportunity for innovative drugs and multinationals will need to participate in that market, despite weak intellectual property (IP) protection and limited options to domestically source product in China - both incentives for national companies to enter and compete with preferential consideration on the NRDL,’ Deere says.

‘Considering that NRDL inclusion will require substantial discounting, at a time when global price transparency is increasingly problematic, as well as intransigent geopolitical tension, multinationals are going to have to employ a very specific and insular Chinese strategy, independent of the western markets.’

Filling the research gap

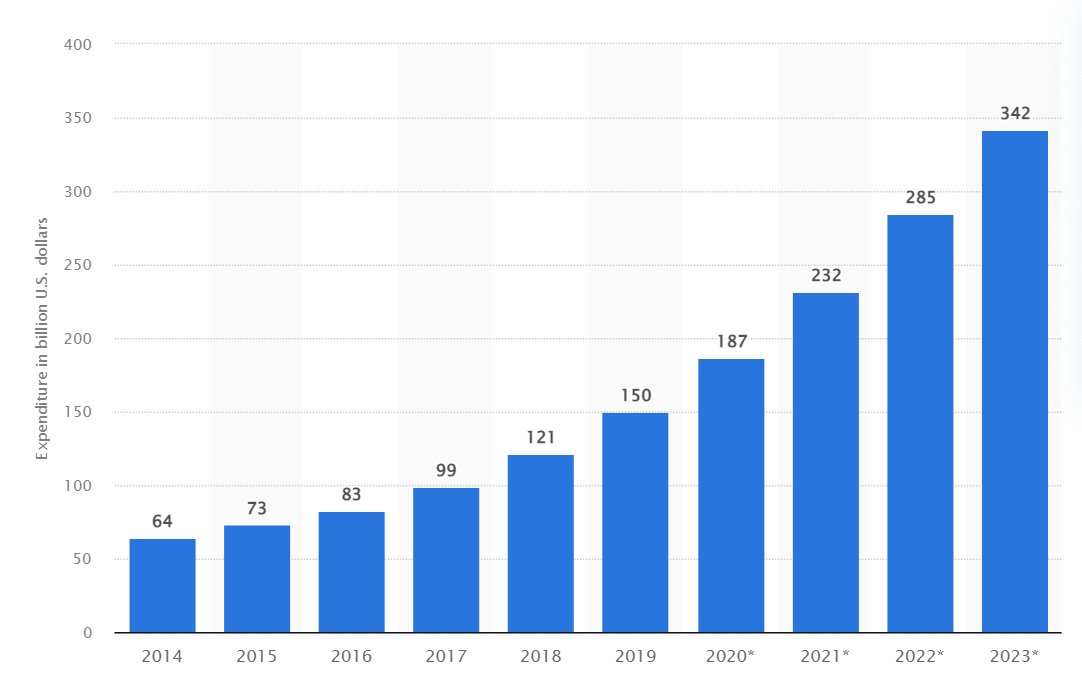

With a pricing and access environment that favours innovation, it should come as no surprise that R&D spending has been consistently rising in China. So much so that it is predicted to reach USD 342 billion in 2023, showing a faster growth than the worldwide average[vii].

Chinese R&D spending (2014-2023) - Source: Statista

In the government’s 14th Five-Year Plan, Chinese pharmaceutical companies were encouraged to ‘become leaders in innovation’ for the first time rather than to ‘follow innovation’, as had been the norm. The government set the goal of a 10% average annual increase in R&D investment and encouraged external investment in Chinese pharma[viii].

The development of immune checkpoint inhibitors (ICIs) has been an especially strong focus of China’s R&D strategy, with these expensive agents being utilised across an increasing number of oncology indications. Multiple domestically developed ICIs have now obtained approval from the NMPA and several more are in the pre-registration phase, waiting for regulatory approval. Second-generation ICIs developed in China offer a significant price advantage over Western-developed, first-in-class equivalents as their inclusion on the NRDL results in significant discounts[ix]. Domestically developed ICIs are therefore favoured when it comes to NRDL inclusion. For the past three years, foreign-made PD-1/L1 inhibitors Opdivo (Bristol-Myers Squibb), Keytruda (Merck Sharp & Dohme) and Imfinzi (AstraZeneca) have been excluded from the NRDL, but three domestically developed PD-1 inhibitors were added to the list last year.

It should therefore come as no surprise that domestic competition in China’s PD-1/L1 inhibitor space is expected to grow rapidly in the coming years, while the Chinese market is expected to be a diminishing source of ICI revenue for Western pharma companies.

Developments in the PD-1/L1 inhibitor arena highlight a central feature of Chinese innovation in the current climate – the tendency to use second-in-class therapies as a commercially-fruitful fallback, while bringing fewer first-in-class therapies to market than western drugmakers.

According to Vicky Xia, this risk-averse approach has been partially caused by a slump in the IPO environment and a resultant dip in investment capital.

‘They [Chinese pharma companies] are still going after relatively “known” targets. That means these targets are already in United States and the Chinese are fast followers,’ Xia says.

‘People are feeling the pressure of less money coming in through the capital markets. [First-in-class drugs] are highly risky and drugmakers can lose a lot of money during clinical trials. Many feel they cannot afford that. If you want to make an innovative drug, you feel that you have to rely on your own strength. And there isn’t much financing available because the climate isn’t that good for biotechs now.’

After reaching record highs in 2021, the biotech IPO market cooled considerably in China this year, in line with wider global trends. In H1 2022, there were 630 IPOs that raised USD 95.4 billion, which represented a fall of 46% and 58% respectively year-on-year. However, the Chinese market has continued to be a key driver for IPO activity, accounting for more than 30% of global public offerings in terms of volume this year[xi].

Regulatory incompatibility

It is impossible to talk about Chinese innovation without spotlighting the difficulties faced by companies seeking regulatory approval in the United States and European Union. Earlier this year, the US Food and Drug Administration (FDA) rejected the lung cancer drug (sintilimab), made by Eli Lilly and partner Innovent Biologics, because it was only studied in China. The regulator called for an additional multi-regional clinical trial that would be ‘more applicable to the US population.’ In May, Hutchmed’s treatment for neuroendocrine tumours was rejected for the same reason, with the FDA again recommending a multi-regional trial[xii].

Speaking about the Eli Lilly-Innovent decision, David Deere notes: ‘What it really boiled down to, was the FDA did not have purview nor access to inspect the clinical trial sites. Clinical development was domestically Chinese, and the protocols did not incorporate a comparator that was the international standard of therapy at the time.

‘So, the FDA used them [Eli Lilly and Innovent] to make an example - they’re not going to approve any drugs where clinical development does not include multi-regional trial sites, open and complete transparency and regulatory access including to trial and commercial source manufacturing sites.’

These core issues - trial diversity and transparency - are at the heart of Chinese drugmakers’ struggle to obtain US and EU approval. And without greater collaboration, standardisation and information sharing, this regulatory tension will likely continue.

‘Going native’ with a China-focused enterprise

To minimise these challenges with regulatory approval, some analysts suggest that multinational corporations (MNCs) should separate their Western and Chinese operations, having their Chinese operation focus solely on the domestic market.

David Deere suggests that MNCs would be prudent to have ‘a strategic plan B for how they can participate in the China market as a Sino-focused enterprise in order to optimise opportunities.’

‘Having separate operations also serves a dual purpose of “arms length” transactions and management if geopolitics deteriorates,’ he says.

‘Running an MNC's Chinese affiliate as a domestically focused operation could also allow an enhanced focus on separate clinical development of "national/regional" therapeutics that cater to the economics of China and similar markets. In reality, it minimizes patent and process technology IP threats, US-FDA/EU-EMA regulatory incompatibility and the risk of adverse effects including manufacturing and sourcing,’ he says.

Looking forward

Though the Chinese market poses its own distinct challenges, its immense size means that multinationals must capitalise on market opportunities wherever they can. According to David Deere, China is the ‘single greatest generational opportunity for Big Pharma’, despite the issues around regulatory incompatibility.

Deere says: ‘China alone is larger than the rest of the emerging markets, combined, and represents the future of the global pharmaceutical industry. In terms of market opportunity, period, it’s huge.’

‘And they're taking all the correct steps. The government is working as quickly as it can to ensure access to their patients. Now the price is dropping through the floor and there's a formal procedure that they use for generics and a procedure they use for innovative products. So, for any multinational - they must play in China.’

Going forward, we are likely to see more funding flow towards R&D as China seeks to shed its reputation as a supply market for ingredients and generic finished drugs and reimagines itself as a hub for innovation.

In a recent Deloitte report on Chinese biopharma, the authors gave several recommendations for Chinese firms entering this era, including ‘conducting more basic research, working harder to commercialize research achievements, facilitating cooperation between the government and investment institutions to inject funds effectively, and building a robust talent pipeline[xiii].’

To realise the full potential of Chinese innovation, domestic firms must embrace R&D - moving away from me-too products and creating first-in-class therapies that are tested in multi-regional clinical trials, as well as securing that innovation with meaningful IP protection. Meanwhile, MNCs would be wise to capitalise on China’s pro-innovation price rules and focus on the opportunities present in its emerging biopharma space.

References

[i] https://www.pharmexec.com/view/maximizing-china-access-for-innovative-therapies

[ii] https://www.s-ge.com/en/publication/fact-sheet/20214-c3-china-medtech-opportunities-hainan

[iii] https://www.pharmexec.com/view/maximizing-china-access-for-innovative-therapies

[iv] https://www.chinadailyhk.com/article/268232#Medical-Connect-program-in-GBA-brings-benefits

[v] https://remapconsulting.com/may-nrdl-china/

[viii] https://daxueconsulting.com/pharmaceutical-industry-china/

[ix] https://www.clinicaltrialsarena.com/comment/domestic-chinese-checkpoint-inhibitors/

Related News

-

News Biotheus partners with BioNTech to take their anti-tumour therapy global

Innovative biotech company Biotheus has signed a deal with BioNTech to manufacture, market, and distribute their latest anti-tumour therapy around the world. -

News Roche acquires rights to Zion Pharma's HER2-positive breast cancer therapeutic

Roche launches into a new agreement with Zion Pharma, a leading Chinese pharmaceutical company, to help develop and commercialise their flagship small molecule tyrosine kinase inhibitor, ZN-A-1041. -

News 2023 Lunar New Year Round-up: Biopharma in the APAC region

With the Lunar New Year ushering in celebrations for the pharmaceutical community around the world on Sunday January 22, 2023, we’ve rounded up some of the top CPHI Online articles and reports from the last year looking at pharmaceutical markets ... -

.png)

News Lonza start commercial operations in newly expanded facility

Lonza Small Molecules adds new capabilities to their expanded facility in China, enabling smoother transitions between small and large scale manufacturing. -

News Thermo Fisher Scientific expands with state-of-the-art facility in China

Thermo Fisher Scientific are to open a new cGMP facility in China, including the latest technology so that they can assist in the accelerated provision of medicines to patients. -

News Sharp seeks greater foothold in Chinese market through ClinsChain partnership

Sharp hopes teaming up with clinical service provider ClinsChain will open the door to the Chinese market -

News WuXi STA launches new HPAPI production facility in China

The new plant features flow chemistry and milling technology, as well as reactors up to 3,000 liters -

News Mitigating supply risk: Having feet on the ground during COVID-19

Having personnel on the ground may be central to mitigating supply chain risks, even as the world embraces the remote approach.

Position your company at the heart of the global Pharma industry with a CPHI Online membership

-

Your products and solutions visible to thousands of visitors within the largest Pharma marketplace

-

Generate high-quality, engaged leads for your business, all year round

-

Promote your business as the industry’s thought-leader by hosting your reports, brochures and videos within your profile

-

Your company’s profile boosted at all participating CPHI events

-

An easy-to-use platform with a detailed dashboard showing your leads and performance