Innovation in Drug Delivery - Part One: The trend towards self-administration

By Yifei Chen and Yasemin Bettina Karanis, IQVIA

In the greater context of the patient journey, more emphasis is often assigned to molecular innovation, rather than the delivery of the drug.

However, in the face of the COVID-19 pandemic, pharmaceutical and drug delivery companies have had to respond to capacity constraints of the healthcare system. One such change is that patient visits have plunged during the peak of the pandemic and levels have still not recovered to full capacity, as seen by IQVIA’s EU5 physicians’ survey. Mechanisms to improve medicine access and delivery for patients, such as moving toward self-administered rather than hospital-administered formulations, therefore will enter the priority lists for the industry.

Here we survey IQVIA’s MIDAS database, examining five-year trends (between 2015 and 2020) of injectable medicine sales data in different formulations. These are sorted by NFC123 codes, and injectables are defined as ampoules, infusions, pens and cartridges, prefilled syringes, and vials. From within, we defined self-administered and hospital-administered drugs based on NFC23 codes. The investigation spans across top therapy areas for injectables, and centre on what drives utilisation and growth toward self-administered drugs.

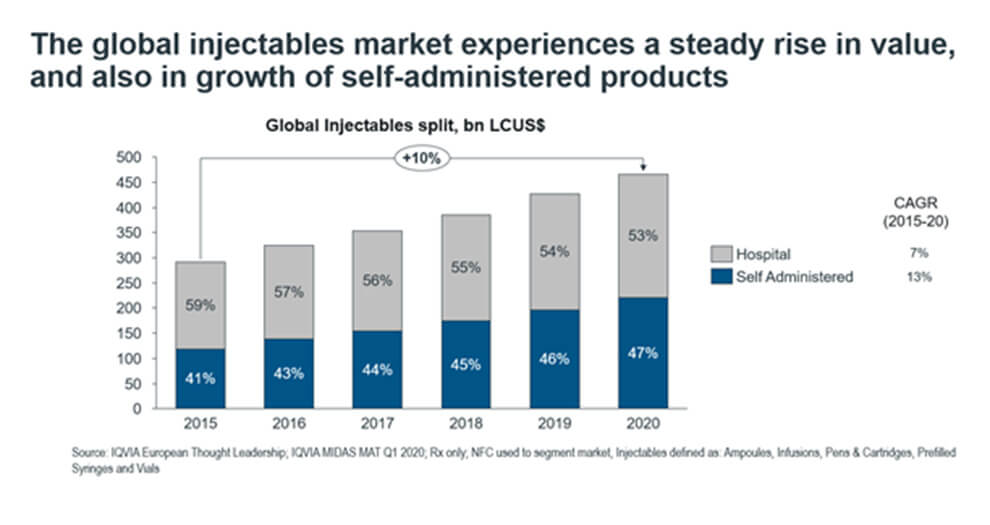

Figure 1. The split in global injectables market into hospital- and self-administered forms

From Figure 1, we see that self-administered injectables demonstrate growth both in relative and absolute terms, from occupying 41% ($119bn LCUSD) of the market in 2015 to 47% ($221bn LCUSD) in 2020. Within the injectables market, self-administered forms are emerging as important drug delivery systems, outpacing the overall injectables market growth with a 13% CAGR.

From Figure 1, we see that self-administered injectables demonstrate growth both in relative and absolute terms, from occupying 41% ($119bn LCUSD) of the market in 2015 to 47% ($221bn LCUSD) in 2020. Within the injectables market, self-administered forms are emerging as important drug delivery systems, outpacing the overall injectables market growth with a 13% CAGR.

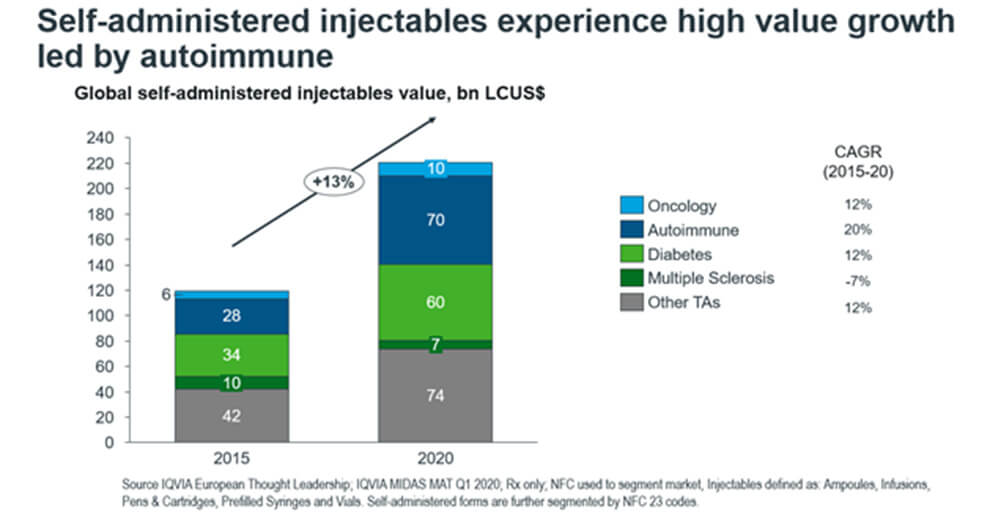

Figure 2. The split in self-administered injectables market into top therapy areas

In Figure 2, we take a deeper look into the top therapy areas for injectables to see which drive growth. The top performing therapy areas are autoimmune, antidiabetics, oncology, and multiple sclerosis. Autoimmune and diabetes drugs dominate the market share by far, with a combined worth of $130 bn. Growth is also driven by the autoimmune segment, which comprises the largest CAGR of 20% and the largest market share of $70bn. Across the past five years, it singly contributes to 41% of the overall self-administered growth.

In our next article, we will take a closer look at the therapy area dynamics for self-administered forms of injectables.

For more information on trends in packaging and devices, please email [email protected]

Related News

-

News Patients vs Pharma – who will the Inflation Reduction Act affect the most?

The Inflation Reduction Act brought in by the Biden administration in 2022 aims to give better and more equitable access to healthcare in the USA. However, pharma companies are now concerned about the other potential costs of such legislation. -

News CPHI Podcast Series: What does the changing US Pharma market mean for industry and patients alike?

In this week's episode of the CPHI Podcast Series Lucy Chard, Digital Editor for CPHI Online is joined by James Manser to discuss the political and market changes in the US pharma field. -

News CPHI Barcelona Annual Report illuminates industry trends for 2024

The CPHI Annual Survey comes into it’s 7th year to report on the predicted trends for 2024. Over 250 pharma executives were asked 35 questions, with their answers informing the industry landscape for the next year, spanning all major pharma marke... -

News Which 10 drugs are open to price negotiation with Medicare in the USA?

The Centres for Medicare & Medicaid Services, under the Biden administration in the USA, has released a list of the 10 drugs that will be open to price negotiations as part of the new legislation under the Inflation Reduction Act (IRA). -

News EU Medical Devices Regulation causes unintended disappearances of medical devices for children, doctors state

Doctor groups and associations have appealed to the EU to correct the EU Medical Devices Regulation law that may cause unintended shortages of essential drug and medical devices for children and rare disease patients. -

News 10 Major Drug Approvals So Far in 2023

Last year, 37 novel drugs were approved by the FDA, this was a high number for such a category, and covered many fields including oncology, demonstrating how promising further research is, and how it is only continuing to build. To date, there are alre... -

News Detecting Alzheimer's disease with a simple lateral flow test

A novel rapid diagnostic test for early-stage Alzheimer's disease has been developed using a biomarker binder from Aptamer Group along with technology from Neuro-Bio, the neurodegenerative disease experts. -

News CPHI Podcast Series: outsourcing and manufacturing trends

Listen to the CPHI Podcast Series this June to hear Gil Roth of the PBOA speak with Digital Editor Lucy Chard about the biggest trends and topics to watch in pharma outsourcing and manufacturing at the minute.

Position your company at the heart of the global Pharma industry with a CPHI Online membership

-

Your products and solutions visible to thousands of visitors within the largest Pharma marketplace

-

Generate high-quality, engaged leads for your business, all year round

-

Promote your business as the industry’s thought-leader by hosting your reports, brochures and videos within your profile

-

Your company’s profile boosted at all participating CPHI events

-

An easy-to-use platform with a detailed dashboard showing your leads and performance